A Behavioral Economics Perspective on Scarcity and Growth

Introduction – Why Saving Alone Won’t Change Tomorrow

Inflation is no joke these days.

You check your credit card bill and sigh, close your food delivery app, cancel a few subscriptions… Saving, of course, is necessary. But here’s the truth: saving alone is not a long-term solution.

Why? Because saving helps you survive today, but it doesn’t transform tomorrow. Over time, excessive frugality erodes your energy and peace of mind. Behavioral science calls this phenomenon “scarcity tunneling.” When your brain is preoccupied with bills due tomorrow, you lose sight of the bigger levers—negotiating a raise, upskilling, or building a side income.

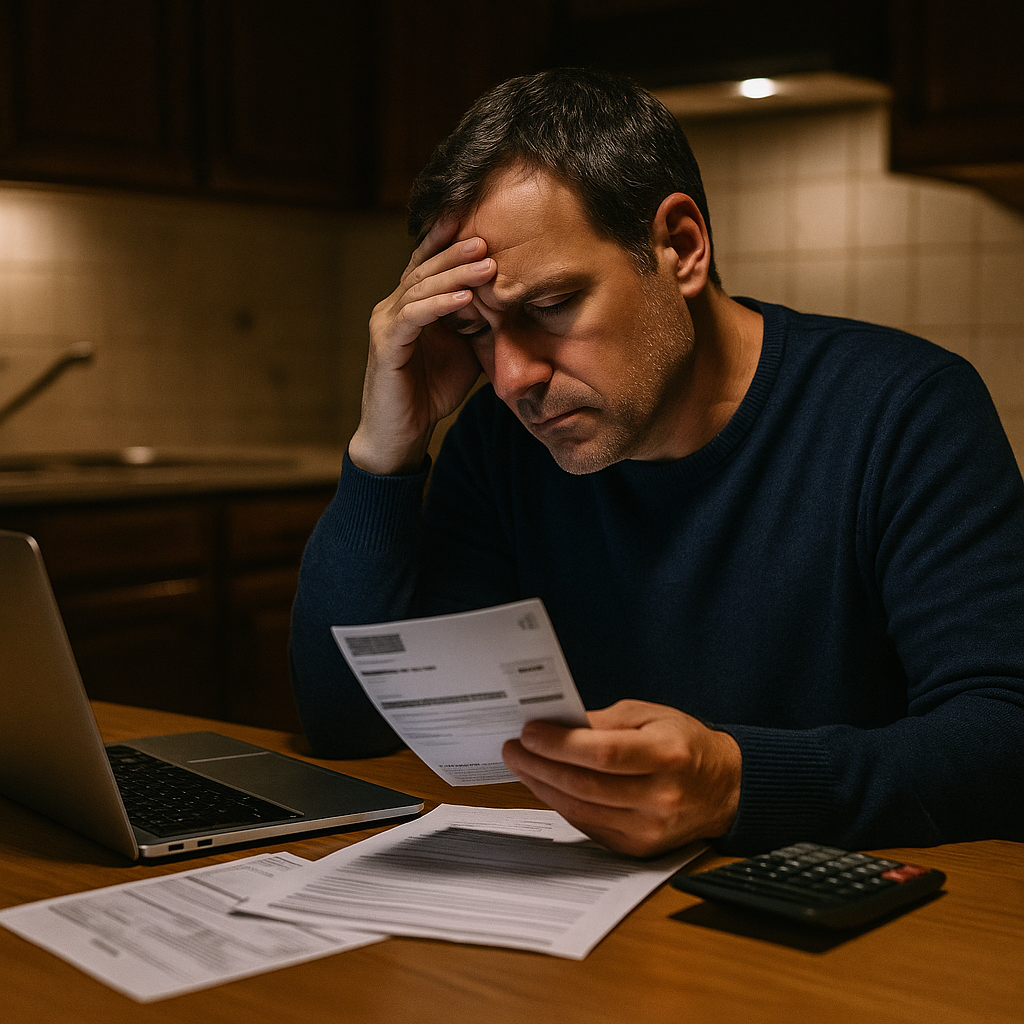

Case Study – The Cost of Over-Saving

John Miller (45, New Jersey) recently noticed his household budget tightening. So he called a family meeting:

“No more eating out. No coffee runs. Netflix is canceled.”

For the first month, it felt manageable—the bank account breathed a little.

But after two, three months, the atmosphere at home turned heavy.

His teenage daughter asked, “Dad, is ramen really all we’re having on my birthday?”

His wife sighed, “These days, all we talk about is money.”

Meanwhile, at work, performance review season arrived.

His manager asked, “John, have you prepared your case for the salary discussion?”

John hesitated: “Honestly, I’ve been too stressed to put it together…”

This is scarcity tunneling at work: financial stress narrows mental bandwidth, lowering productivity and straining relationships. Data confirms that chronic frugality correlates with higher household conflict and weaker job performance.

Saving = Brakes, Income Growth = Accelerator

You can’t reach your destination by pressing the brakes alone.

Use saving as a short-term measure to buy time, but shift your energy toward stepping on the accelerator: income growth.

A Simple Comparison

- Saving Scenario: Cutting $120/month → $1,440/year

- Earning Scenario A: 5 hours/week tutoring, freelancing, or delivery → +$250/month → $3,000/year

- Earning Scenario B: 10% raise on a $3,000/month take-home salary → +$300/month → $3,600/year, and this increase compounds into the future.

Both are realistic, but the compounding power of earning is far greater. Raises, higher rates, or new skills stack year after year. Research also shows that higher income improves subjective well-being more effectively than prolonged cost-cutting.

The Hidden Costs of Long-Term Frugality

- Tunnel Vision Focusing on $5 or $10 savings consumes all your energy while you miss bigger wins (raises, job changes, skill investments).

- Relationship Strain Money talk often turns into conflict. Extended austerity mode raises family and workplace tensions.

- Mental Health Deterioration Financial stress is strongly linked with anxiety and depression.

How to Step on the Accelerator – A 4-Week Transition Plan

Week 1 | Organize Your Numbers (2 hours)

- Separate fixed vs. variable costs. Cut only “painless fat” (unused subscriptions, duplicate data plans). Stop there.

Week 2 | Build Your Case to Raise Prices or Salary (5 hours)

- Summarize work achievements (metrics, customer feedback, completed projects). Freelancers: update portfolio and references.

Week 3 | Market Research & Negotiation Prep (4 hours)

- Research salary bands or market rates in your field. Prepare for raise/fee negotiations.

Week 4 | Launch One Immediate Side Income (5 hours)

- Start a monetizable activity with existing skills:

- Weekly coaching sessions

- Listing a product/service online

- Weekend freelance work with higher hourly pay

- Remember: “Start small → test fast → scale.”

The formula is: time-limited saving + immediate earning + long-term base growth.

Short Conversations, Long Lessons

At a bar, a friend told John:

“You’ve got to save. Everyone’s cutting back these days.”

John nodded, then replied quietly:

“Sure, I’ll cut back for now. But this month, I’m negotiating a raise and taking on a weekend gig. This isn’t stopping—it’s accelerating.”

Is that true? Absolutely. Saving is the brake, income is the accelerator. And the car only moves forward when you press the accelerator.

Key Takeaways

- Saving is short-term and temporary, a survival tool.

- Income growth is long-term and structural, reshaping your financial trajectory.

- The less money you have, the more important it is to focus on earning rather than only cutting.

- Always put an expiration date on austerity. Once it ends, switch gears and accelerate.