What Compounding Really Means (and Why 12% Is Transformative)

Compounding is not just “interest on interest”—it’s the engine that scales time into wealth. At 12% annual returns, the effect is dramatic: the curve looks flat for years, then explodes. That back-loaded growth is why starting early (not starting big) is the single most important decision.

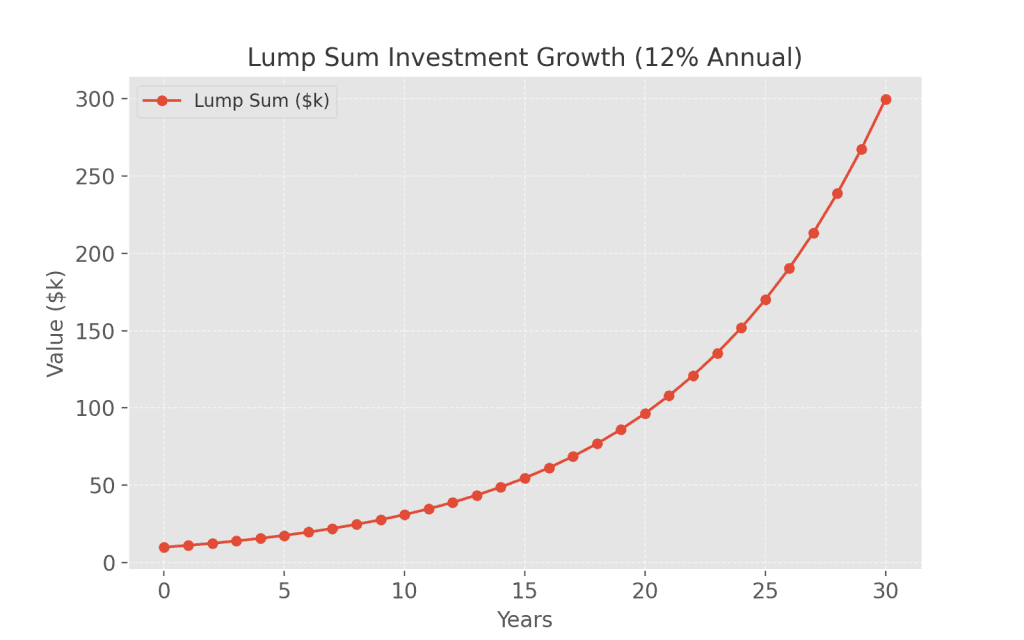

Example 1 — Lump-Sum: $10,000 at 12% (Annual Compounding)

If you place $10,000 and let it compound annually at 12%:

10 years → about $31,058

20 years → about $96,460

30 years → about $299,600

The last 10 years added more than the first 20 combined. That’s the time effect in action.

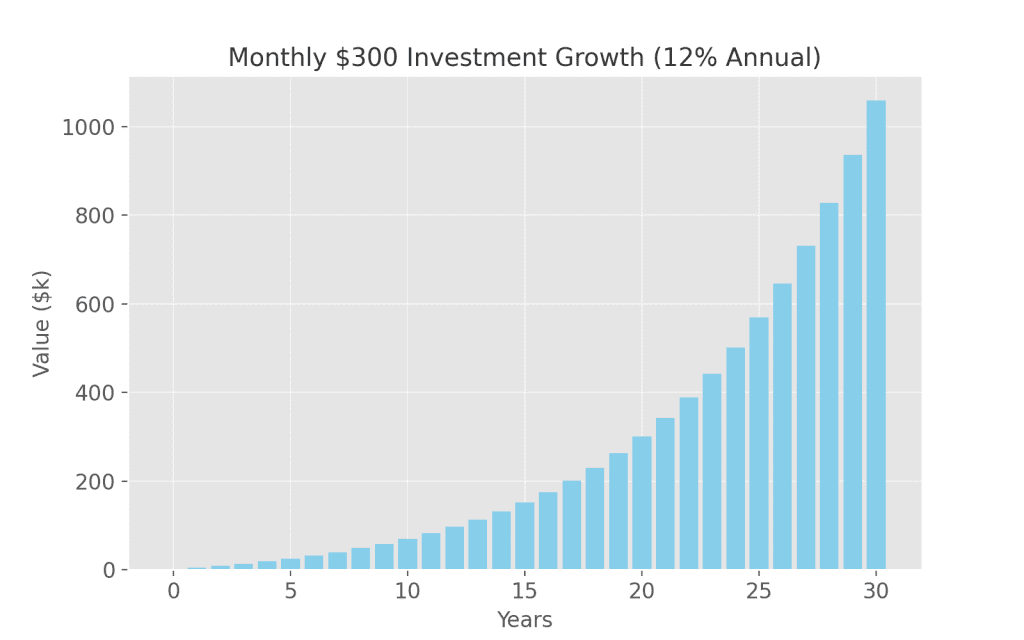

Example 2 — DCA: $300/Month at 12% (Monthly Compounding)

Contributing $300 at the start of each month and compounding monthly at 12% for 30 years builds roughly low-seven figures. A steady drip outperforms sporadic, larger deposits because the time-in-market multiplies every contribution.

Practical levers

Auto-invest monthly (don’t rely on willpower).

Reinvest dividends (turn distributions into fuel).

Avoid interruptions (see “pitfalls” below).

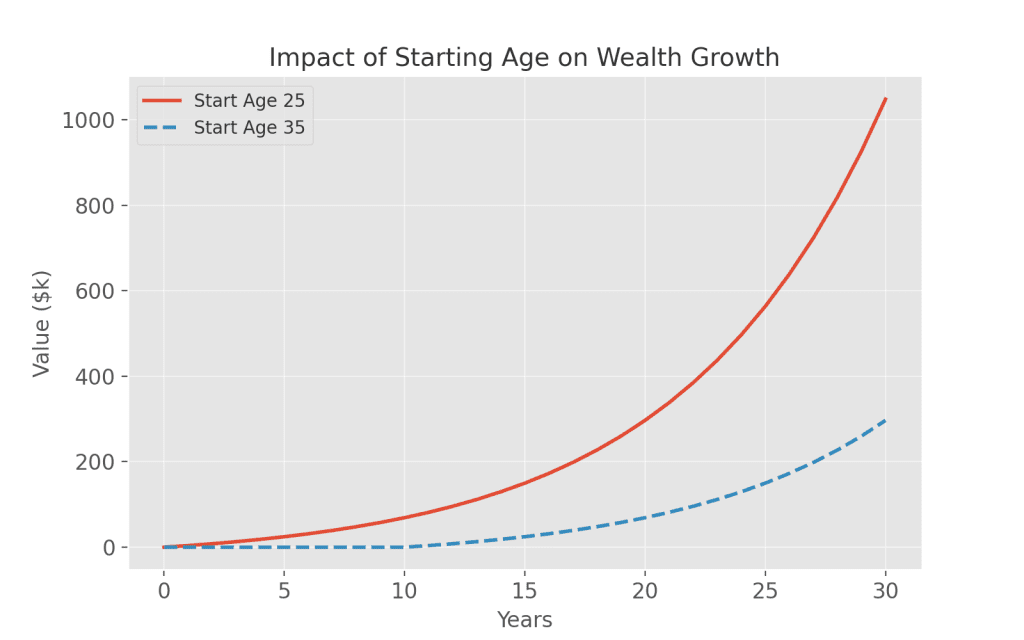

Example 3 — The Real Cost of Delay: Start at 25 vs 35 (Both to 65)

Same $300/month, same 12%, one difference: when you start.

Start at 25 (40 years) → ends in the multi-million range

Start at 35 (30 years) → ends around low-seven figures

Even though both investors follow the rules, the 10-year delay costs well over $2M at 12%. Starting early is mathematically irreplaceable.

Example 4 — Fee Drag: Why 1% Matters More Than You Think

Fees look small; compounding makes them huge. Compare a 30-year plan (initial $10,000 + $300/month):

12% net → ~$1.44M

11% net (just 1% fee drag) → ~$1.13M

Wealth lost to fees → $300k+

Table:“Fee Drag – 12% vs 11% over 30 years”

Takeaway: Attack recurring costs. A 1% fee difference can erase hundreds of thousands over decades.

Rule of 72 (Quick Intuition)

At ~12%, money doubles every ~6 years (72 ÷ 12 = 6). That’s why the last decade dominates the total.

Pitfalls That Break Compounding

Stopping contributions during drawdowns (you cancel your best future multipliers).

High fees and friction (advisory fees, trading churn).

Cash drag (idle cash not compounding).

Tax inefficiency (realizing gains too often; use tax-efficient wrappers where possible).